FA News – 14th June 2022

Medical aid is essential for accessing private healthcare in South Africa, but when children become adults, the rate charged for being a dependent on their parents’ medical aid increases substantially. However, many young adults are still studying, or are working entry-level jobs and simply cannot afford to become the primary member on their own medical aid.

Downgrading the medical aid plan seems to be an option for saving money so that parents can continue to pay for their children, but this also results in reduced cover that may mean they pay shortfalls they would not have before. Cancelling medical aid altogether may also appear to be an attractive option, especially if you are young and healthy, however accidents and illness can happen to anyone at any time, regardless of your age.

While it is tempting to simply cancel medical aid cover when this seems to be a burdensome and unnecessary expense every month, this could leave you in even more dire financial straits should something happen. Breaks in medical aid cover as an adult mean that waiting periods can be enforced when you re-join, and if you stay without cover until you are over age 35, there will be late joiner penalties imposed on the premiums for life.

So, what is the answer? Joanne Stroebel, Medical Aid Specialist at JST Consulting, explains that every family is different, so it is critical to talk to a financial advisor to find the best solution to meet your needs.

“When children turn 21, they are typically considered adults, although some medical schemes allow child dependents until age 25. However, it is less expensive to remain as an adult dependent than to be the primary member. If you earn less than R10 000 a month, however, there are low-income options available that may be less expensive. The key is to find the balance of a cost-effective solution that still offers the cover you need, and gap cover forms an important part of a holistic portfolio,” she says.

The reality is that accidents happen to everyone, even if you are young and healthy, and dread diseases like cancer are seeing massive increases in numbers in people aged 35 and under. Your broker can help you to find a solution that works for you. You may not need the day-to-day benefits of comprehensive cover, so a hospital plan for accidents and planned treatments may be an option. Combining this with gap cover to cover many of the shortfalls members experience on these plans can ensure that should you require medical attention, you won’t be paying for it for the rest of your life.

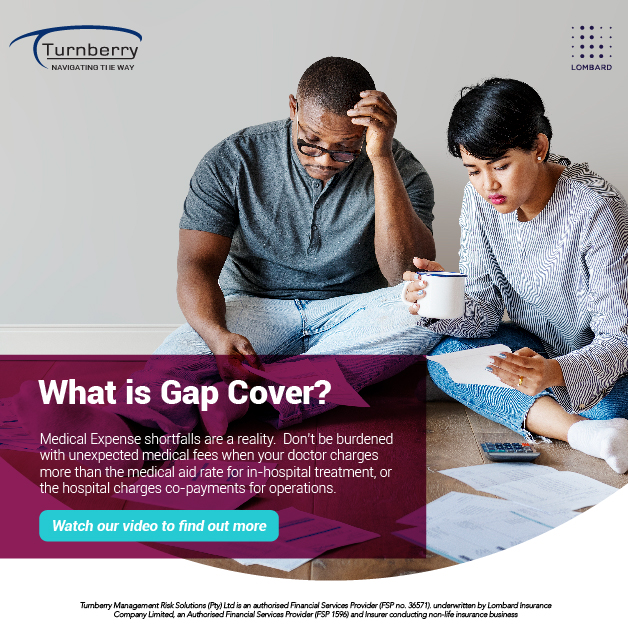

“There is often a significant difference between what medical practitioners and hospitals charge, and what medical aid schemes will pay out. On a hospital plan, this is generally 100% of the medical aid tariff, and most doctors charge 200% or 300% of this, with specialists going up to 500% of the rate. Gap cover is exactly what it sounds like – insurance that covers this gap, which can be a financial lifesaver in the event of severe illness or accidents,” says Tony Singleton, CEO of Turnberry.

Medical aid may be a luxury, but it is one that has become vital for many South Africans, as state healthcare facilities often have long waiting periods, especially for elective surgeries and treatment for illnesses like cancer. Being a member of a medical aid gives you access to treatment at private facilities, even if these are within a specified network, as well as Prescribed Minimum Benefit (PMB) conditions.

Reducing medical aid premiums by opting for basic cover through a hospital plan, and then bolstering this with affordable gap cover solutions, may be a good solution for many young people as they come off their parents’ medical aid plans.

However, when it comes to making any decisions that involve your future financial health, a financial advisor is an excellent resource. They can help you find the most cost-effective options for your circumstances, so that you don’t end up in massive debt should you require surgery or treatment for a dread disease.

https://getcovered.turnberry.co.za/app/1

What is Gap Cover?

https://getcovered.turnberry.co.za/app/1

Client Testimonials

Turnberry assisted with claims for various incidents during the last few years – from an elective orthopaedic surgery for my young daughter to emergency surgeries for my wife. When my wife was diagnosed with cancer last year, the once-off payment assisted in a number of the out-of-hospital expenses. In addition, the knowledge that the expenses threshold is so much higher than the standard medical rates provided peace of mind. I have recommended Turnberry Gap Cover to our family, and reiterate that it is an essential or mandatory product. No healthy person believes critical or emergency procedures will happen. But the truth is that it can happen to anyone. The cost vs benefit is not a logical debate, without gap coverage you may end up selling assets to cover the bills. Turnberry’s services were professional, quick and efficient – ‘Peace of mind’. Mynhardt Oosthuizen – January 2022